Table of Contents

JAIIB Paper 2 (PPB) Module B Unit 2: Appraisal and Assessment of Credit Facilities (New Syllabus)

The Institute of Indian Banking and Finance (IIBF) has recently announced the revised syllabus and exam format for the JAIIB Exam 2023. The upcoming exam will comprise of four papers, with Paper 2 (Principles & Practices of Banking) covering Unit 2: Appraisal and Assessment of Credit Facilities. This particular unit holds significant importance for candidates, as it will greatly impact their performance in the exam.

To assist candidates in comprehending the topic, we will provide all the necessary details related to Unit 2: Appraisal and Assessment of Credit Facilities of JAIIB Paper 2 (PPB) Module B: Functions of Banks. We strongly recommend candidates to refer to this article and also utilize our Online Mock Test Series to enhance their understanding of Foreign Currency Accounts for Residents and other related aspects.

For candidates appearing for the JAIIB Certification Examination 2023, it is essential to comprehend each unit in the syllabus, including the Marketing unit. This unit holds great importance in the banking industry, and candidates must prepare thoroughly to excel in the exam and establish a successful career in the banking sector.

Credit Appraisal Process

Credit Risk and Rating

- Credit risk is defined as the possibility of borrower/counterparty default. Default can occur because of business failure or because the borrower’s willful actions.

- Lenders rely on credit reports for individual borrowers and credit rating of companies/firms by the rating agencies and their own credit rating.

- Credit risk rating is one of the credit appraisal tools. In this method credit risk is assessed in the form rating by assigning marks to different parameters and evaluating on the basis of some threshold preset standards/marks. The borrower’s financial standing and performance are rated for scoring.

Aspects Of Appraisal

Aspects of Appraisal

Aspects of Appraisal

There are four cardinal parameters of lending. These are as follows:

- Evaluation of creditworthiness of the borrower

- Considering the purpose of the loan

- Verifying the cash flows and source of repayment

- Assessing the security/collateral security.

Methods of Assessment of Loan

Assessment of loans for different purposes is done in different manner as the factors affecting these differ in several respects. Broadly, these can be categorized in the following types:

Loans for business enterprises:

- For Working Capital Purposes

- For Capital Expenditure

Loans for individuals:

- For Housing Purposes

- For Vehicles/ Consumer Durables

Assessment Of Working Capital

Working Capital

The capital required for a business enterprise can be classified under two main categories

- Fixed Capital

- Working Capital

Working capital refers to that part of the firm’s funds that is required for financing short-term or current assets such as cash, debtors & inventories.

There are two concepts of working capital:

- Gross working capital

- Net working capital

Gross Working Capital

It is the capital invested in total current assets of the enterprise. Current assets are tangible movable assets that are recoverable in cash or sold or consumed or turned over during the operating cycle usually not exceeding one year.

The merits of gross concept are:

- Enables the enterprise to provide correct amount of working capital at the right time

- Helps management to know the amount invested in total current assets with which it has to operate.

Net Working Capital

The net working capital (NWC) or liquid surplus is the difference between current assets and current liabilities.

The net working capital should be higher than 1:1 to ensure sufficient liquidity and availability of working funds.

The net working capital concept, however, is also important for following reasons:

- It is qualitative concept, which indicates the firm’s ability to meet to its operating expenses and short-term liabilities.

- It indicates the margin of protection available to the short term creditors.

Working Capital group

- It is a concept used in the Indian banking sector to determine the amount of working capital limits the bank would make available to the borrower. It is the difference between total Current Assets and Current Liabilities, other than bank borrowings.

Components of Working Capital

Working capital is the aggregate value of:

- Raw material

- Stock in process

- Finished goods in stores and in transit

- Other consumable stores

- Receivables or sundry debtors

- Other expenses

Operating / Working Capital Cycle

The duration from the purchase of raw materials through production to finished goods to sales and sales realisation is the time period for which working capital funds are required. Once sales proceeds are received in cash, this money is available for purchase of raw materials and continuing production. The whole process is repeated again. Because of the cyclical nature of this entire process, the production period is called the operating cycle.

Computation of Operating Cycle Components

Assessment of Working Capital Requirements

Banks may adopt one of the following four methods for assessment of working capital requirements of their clients.

- Turnover Method

- Operating Cycle Method

- Maximum Permissible Bank Finance (MPBF) Method

- Cash Budget Method.

These methods require the preparation of: (a) Projected financial statements (b) Projected fund flow statements (c) Projected cash flow statements/cash budgets

Turnover Method

- MSE units having working capital limits of up to Rs. 5 crore from the banking system are to be provided working capital finance computed on the basis of 20% of their projected annual turnover.

- Under this method, the working capital requirements of the borrower is computed at 25% of the projected annual turnover of which normally 20% of the projected turnover is provided by the bank as working capital finance and balance 5% of the projected annual turnover is contributed by the borrower, as margin towards working capital.

- While the working capital limits are fixed based on the assessment exercise, the actual drawings are permitted based on the level of current assets viz. stock and debtors less the security margin fixed for the respective assets.

Illustration:

M/s. ABC is a manufacturer of moulded plastic household goods like buckets, mugs etc. The annual turnover for FY2021-22 was `80.00 lakh, and it has targeted 25% growth in FY 2022-23. The working capital requirement and the bank finance for it are estimated as follows.

- Growth in turnover during FY2022-23 @ 25% over FY2021-22: `80.00 lakh * 0.25 = `20.00 lakh

- Projected turnover during FY2022-23: `80.00 lakh + `20.00 lakh = `100.00 lakh

- Working capital requirement @ 25% of turnover: `100.00 lakh* 0.25 = `25.00 lakh

- Bank finance for working capital @ four-fifth (i.e. 80%) of (c) = `25.00 lakh * 0.8 = `20.00 lakh

- Borrower’s contribution for working capital @ one-fifth (i.e. 20%) of (c) = `25.00 lakh * 0.2 = `5.00 lakh

Alternatively, the bank finance and the borrower’s contribution for working capital are directly determined from the projected turnover as follows: (a) Bank finance @ 20% of projected turnover = `100.00 lakh* 0.2 = `20.00 lakh (b) Borrower’s contribution@ 5% of projected turnover = `100.00 lakh* 0.05 = `5.00 lakh

Illustration:

M/s. PQR is a manufacturer of toys. The projected annual turnover is `120.00 lakh. The available net working capital (NWC) is `5.00 lakh.

- Projected annual turnover: `120.00 lakh

- Working capital required (25% of a): `30.00 lakh

- Minimum margin from the borrower (20% of b): `6.00 lakh

- Maximum bank borrowing (80% of b): `24.00 lakh

- Actual NWC available: `5.00 lakh (f) Margin stipulated (Higher of c or e): `6.00 lakh

- Permissible limit (b-f): `24.00 lakh

- Additional Margin to be brought in by borrower (c – d): `6 lakh – `5 lakh – `1 lakh

Operating Cycle Method

- It requires estimation of the holding periods of major current assets and current liabilities. If part of raw materials is available on credit, then bank finance will be required only for that portion of the raw materials which represents fully paid purchases. Similarly, if advance payments are received against orders, only that part of the finished goods net of the advance payment will require bank credit.

- Only those debtors whose outstanding is up to a specified period (180 days maximum) are considered.

- If creditors are in excess, the excess portion is deducted from the value of stocks. If debtors are in excess, the bank considers the surplus debtors for financing.

Illustration:

M/s. ABC is in ready-made garments manufacturing activity. The average holding periods for stocks and duration of creditors and debtors are as given below. Its annual turnover is `70 lakh and annual operating expenses are `60 lakh. The working capital requirement is computed as shown below.

- Procurement of raw material: 30 days

- Conversion/process time: 15 days

- Average time of holding of finished goods: 15 days

- Average collection period: 30 days

- Total operating cycle (a + b + c + d): 90 days

- of operating cycles in a year (360/e): 4

- Total operating expenses per annum: `60 lakh

- Total turnover per annum: `70 lakh

- Working capital requirement (g/f): `15 lakh

Maximum Permissible Bank Finance Method

- RBI had constituted a Working Group headed by Shri P.L. Tandon, the then Chairman of PNB, in July 1974. It enunciated the concept of MPBF for assessment of working capital. It suggested different methods of funding current assets to be adopted depending on the size of credit required.

- First Method of Lending: In this method, the contribution by the borrowing unit is fixed at a minimum 25% of the working capital gap from long-term funds. The bank finances a maximum of 75% of the gap; the balance amount should come from long-term sources. This method of lending gives a current ratio of only 1:17. This approach was considered suitable for relatively new units set up by first time entrepreneurs and for sick/weak units.

Maximum Permissible Bank Finance Method

- Second Method of Lending: Under this method, the borrower is required to provide for a minimum of 25% of total current assets out of long-term funds and the bank will provide the balance (MPBF). This would give a minimum current ratio of 1.33:1.

- Third Method of Lending: Under this method, the contribution from long term funds would be to the extent of the entire core current assets and a minimum of 25% of the balance current assets. The balance current assets only would be financed through bank finance for working capital after netting off other current liabilities meeting the current assets.

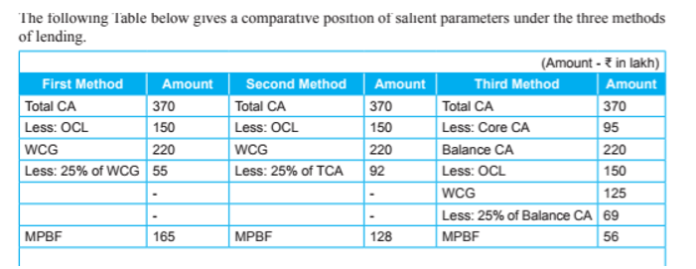

MPBF Method Illustration

Observations

- Under the first method: MPBF is `165 lakh, thus excess borrowing is of ` 35 lakh.

- Under the second method: MPBF is `128 lakh, thus excess borrowing is of ` 72 lakh.

- Current Ratio (after funding excess borrowing through long term sources) is 1.17 (under first method) and 1.33 (under second method) The following Table below gives a comparative position of salient parameters under the three methods of lending.

(i)CMA Data: Many banks continue to follow the method of MPBF based on CMA (Credit Monitoring Arrangement) formats. Various banks use CMA formats with certain variations to suit the requirements of particular industry segment. For example, the CMA formats used for finance to NBFCs are different than those prescribed for a manufacturing company. CMA formats consist of the following forms: FORM I – Particulars of the existing limits from the Banking System/Financial Institutions

FORM I – Particulars of the existing limits from the Banking System/Financial Institutions

FORM II – Operating Statement

FORM III – Analysis of Balance Sheet Part A – Balance Sheet Spread – Analytical and Comparative Ratios.

FORM IV – Comparative statement of current assets and current liabilities

FORM V – Assessment of Maximum Permissible Bank Finance for Working Capital FORM VI – Funds Flow Statement

In addition, the banks also obtain data on the following two formats:

- Format for Salient Financial Indicators

- Format for Additional Information/Additional Data

Cash Budget Method

- Most banks now for assessment of the working capital needs of a borrower who enjoys or requires fund based limits in excess of Rs. 10 crore, adopt the cash budget system.

- A cash budget is a statement of cash receipts and cash payments. Cash budget is a substitute for the operating cycle method for the assessment of working capital.

- Under this method the peak cash deficit amount is the total working capital finance to be provided to the borrower by the bank. The required borrower’s contribution (NWC), which should be at least 25% of the peak deficit, is also worked out based on the values of Current Assets and Current Liabilities as at the peak deficit period. Actual drawings are allowed to the extent of monthly cash deficit.

Advantages of Cash Budget Method

- The customer plans his cash requirements in advance and in case his bank is unable to sanction additional funds, the customer can seek alternative sources well in advance.

- The banker is in close touch with his customers. He would, therefore, be able to spot any danger signals quickly and initiate corrective action in time.

- The banker can plan his resources to meet expected credit demands. Credit planning would thus become a meaningful exercise.

Assessment of Non-Fund Based Facilities

Bank Guarantee

- For assessing bank guarantee required by a borrower, details such as the nature of guarantee, its purpose, the particulars of the contract period and the amount for which the guarantee is sought are collected and assessed from the aspect of creditworthiness of the customer and his relationship with the bank for sanctioning the guarantee facility.

- Bank must clearly understand various types of guarantees required in the line of activity and classify them into Financial and Performance guarantees.

Purpose of Bank Guarantee

- Permanent Guarantees: It is important to identify and segregate those guarantees which are likely to be required on a fixed basis and will be outstanding as long as the unit is in operation or the bank finance is outstanding.

- Business Activity Related Guarantees: The limit for guarantees related to the main business activity of the firm is a function of the volume of activity proposed and the duration of such guarantees.

- Guarantees for Export Quota: the guarantee amount is related to the value of quota applied and allotted, which in turn will depend upon the level of exports proposed in the ensuing year and other factors.

- Guarantees for Tax Liabilities: borrower may require guarantees to be issued favouring Excise, Income-Tax authorities against disputed liabilities.

- Guarantees for Import of Capital Goods: The borrower may also require guarantees for import of capital goods on concessional import duty under various schemes of Government, whose requirement can be determined on a case to case basis.

- Guarantees for Advance Payments: Wherever the borrower is accepting advance payment from purchasers and is required to furnish bank guarantees in lieu thereof, the amount of such guarantees will be proportional to the amount of such advance payments that will be outstanding, which in turn will be dependent on the level of sales.

Assessment of Non-Fund Based Facilities

Letter of credit

- A letter of credit (L/C) is a written but a conditional undertaking given by the issuing bank on behalf of its customer, to the beneficiary that it will pay him the amount stated in the credit provided documents specified in the letter of credit are drawn and presented in strict conformity with the terms and conditions of the credit.

- In order for the payment to occur, the seller has to present to the bank the required documents as per the L/C terms.

Assessment of LOC Limit

For assessing the letter of credit limit for the purchase of raw materials, the banker collects from the borrower following particulars:

- Projected value of raw material consumption in the ensuing year

- Projected value of raw material purchase on credit

- Time taken for advising the letter of credit to the beneficiary

- Time taken for shipment and the consignment to reach the customer’s destination

- Credit period (usance period) agreed between the beneficiary and the customer

- Credit period projected and reckoned for calculation of the maximum permissible bank finance (MPBF) while sanctioning the funded limits to the borrower customer

Assessment of Term Loan

- A term loan is granted for the purpose of acquisition of capital asset. Normally, the term loans are repayable in instalments over a period ranging from 3 to 10 years. The credit risk, therefore, is greater in case of term loan than in case of working capital finance.

- It is necessary to assess the future cash surplus from the business operations that would be available to service the term loan viz. for meeting the interest and repayment instalments for the term loan.

Assessment of Term Loan Limit

- Land and site development

- Building

- Plant and machinery

- Technical know-how

- Expenses on foreign technicians

- Miscellaneous assets

- Preliminary & pre-operative expenses

- Contingencies

- Margin for working capital

- Initial cash losses:

- Sources of Finance: To meet the cost of the project, the following sources of finance are available: − Share capital − Term loans − Debenture capital − Deferred credit − Incentive sources − Miscellaneous sources

Assessing Viability and Debt Servicing Capacity

Viability of Business Activity: Assessing the viability of any business activity is essentially an exercise of working out projected sales and costs of production and cost of sales, etc. In other words, it is preparing projected financial estimates for operations. The objective here is to determine the profits and the cash surplus generated from the operations.

Debt Service Coverage Ratio (DSCR): DSCR indicates the ability of a concern to service its term liabilities. DSCR measures whether interest and instalments can be paid out of internal generation of funds. It is calculated as the cash profit generated plus provision for interest divided by total payment commitment. DSCR of 1.5 is considered reasonable

DSCR = Net profit + Depreciation + Other Non-Cash Expenses + Interest on term loan / (Interest on term loan + Instalments of term loan)

JAIIB PPB Module B Unit 2 Appraisal and Assessment of Credit Facilities (Ambitious Baba) PDF

- Join Telegram Group

- For Mock test and Video Course Visit: test.ambitiousbaba.com

- Join Free Classes: JAIIBCAIIB BABA

- Download APP For Study Material: Click Here

- Download More PDF

Click here to get Free Study Materials Just by Fill this form

Discount Offer Available Visit : test.ambitiousbaba.com

Buy JAIIB MAHACOMBO 2023