Table of Contents

JAIIB Paper 4 (RBWM) Module C Unit 3:Delivery Models (New Syllabus)

The Institute of Indian Banking and Finance (IIBF) has recently announced the new syllabus and exam pattern for the JAIIB Exam 2023. Similar to the current format, JAIIB 2023 will consist of four papers. One of the important topics covered in Paper 4 (Retail Banking and Wealth Management) is “Delivery Models,” which is a crucial unit that every candidate must grasp thoroughly. To ensure that aspirants have a better understanding of the topic, we will provide all the necessary details related to Unit 3: Delivery Models of JAIIB Paper 4 (RBWM) Module C Support Services – Marketing of Banking Services/ Products. We strongly recommend that candidates refer to this article and utilize our Online Mock Test Series to enhance their knowledge of Delivery Models.

Delivery Models

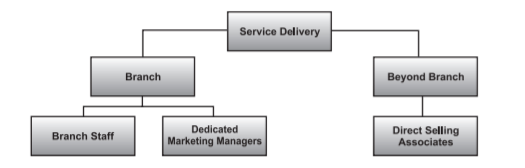

The success of the Retail Banking depends on how the products and services are delivered to the customer. Delivery effectiveness in physical channels is determined more by the persons who are delivering the services.

The three important human interventions in physical channels are

- Internal Customer – Staff of the Branch

- Specialised Marketing Personnel

- Direct Selling Associates (DSAs).

Dedicated Marketing Managers

- Dedicated Marketing Managers were appointed in addition to existing internal human resources.

- These specialist Marketing Managers (MBAs in Marketing) were young and energetic and recruited from the campuses of management Schools.

- Some banks appointed them in Junior Management and some other banks in middle management.

The expectations from these officers are explained:

- Market Intelligence

- Potential Sourcing

- Product and Service Delivery Presentations to the identified customer segments

- Right selling to the targeted customer group

- Sales Conversions

- Closing the leads with sales

- Compliance of promises made and conforming to the services delivery standards

- Following up with the operations department for effective process and delivery of products sold.

Direct Selling Agents (DSAs)

- DSAs are agencies appointed by banks to source business for them on a fee basis.

- DSAs are primarily engaged in sourcing Credit Cards and Retail Loans.

- The employees of the DSAs missell credit card products and make the customers fall into a debt trap by misusing the cards.

- Same is the case with misselling of retail loans and in this space, the pricing for the loans are not explained clearly.

- Ultimately this will result in dissatisfaction for the customers and reputation risk for the bank.

Reputation Risk is always a threatening factor in the DSA model

- DSAs focus on pure selling by pushing the products than effective marketing after verifying the needs of the customers and their actual requirements.

TIE-UP with Institutions/ OEMS/DEALERS ETC….

Banks enter into tie ups with the following agencies for extending different types of loans.

- Tie up with Builders as a preferred financier for extending Home Loans to prospective buyers.

- Tie ups with auto dealers is another method adopted by banks for expanding retail credit.

- Sanctioning of Personal Loans under tie up with different institutions is another model adopted by banks to expand retail loans.

- educational loans are disbursed on a tie up basis. Banks set up special counters during the admission season in reputed educational institutions and offer education loans based on merit.

JAIIB Paper 4 Module C Unit 3 Delivery Models (Ambitious Baba) PDF

- Join Telegram Group

- For Mock test and Video Course Visit: test.ambitiousbaba.com

- Join Free Classes: JAIIBCAIIB BABA

- Download APP For Study Material: Click Here

- Download More PDF

Click here to get Free Study Materials Just by Fill this form

Discount Offer Available Visit : test.ambitiousbaba.com

Buy JAIIB MAHACOMBO 2023