Table of Contents

CAIIB Paper 3 ABFM Module B Unit 6 : Decision Making (New Syllabus)

IIBF has released the New Syllabus Exam Pattern for CAIIB Exam 2023. Following the format of the current exam, CAIIB 2023 will have now four papers. The CAIIB Paper 3 (ADVANCED CONCEPTS OF FINANCIAL MANAGEMENT) includes an important topic called “Decision Making”. Every candidate who are appearing for the CAIIB Certification Examination 2023 must understand each unit included in the syllabus.

In this article, we are going to cover all the necessary details of CAIIB Paper 3 (ABFM) Module B (THE MANAGEMENT PROCESS) Unit 6 : Decision Making, Aspirants must go through this article to better understand the topic, Decision Making and practice using our Online Mock Test Series to strengthen their knowledge of Decision Making. Unit 6 :Decision Making

Decision Making Using Cost-Volume-Profit (CVP) Analysis

- In practical terms, the cost, volume and the price are the important ingredients of any profit analysis.

- Cost has two main components namely, fixed and variable.

- The fixed cost per unit will go down if volume of production or sales increases.

- Variable cost generally varies with volume but here too the variance will depend on the product mix and the processes adopted.

- Higher volume of productions will generally reduce the cost of production due to economy of scale, but incremental cost due to upscaling the facilities may again change the cost structure.

- Higher volume in sales may accompany with disproportionate increase in marketing cost, some of which will be for brand building and the rest may commensurate with the sales volumes.

- While pricing will have direct impact on profitability, it in fact determines the breakeven point.

- Higher the sales realisation, earlier the breakeven point.

- Volume will also have direct impact on absolute profits, which too will be a determining factor in calculating the breakeven point.

- An investor will have many constraints and criteria while taking a decision to invest.

Some important points affecting investment decisions due to cost, volume and price, which ultimately determine profits and the breakeven point, are noted below.

- When we introduce a new product in the market, we cannot expect high volumes and therefore the costing will be higher.

- In the aforesaid scenario, we will have to keep the price affordable or practically low to attract new set of buyers, which will delay the breakeven point.

- In case of a consumer products having large market, we will have to plan for big volumes which will require large capital investment.

- In the aforesaid scenario, to carve out a reasonable market share, huge advertisement and brand building expenses will have to be incurred affecting the cost and profitability.

- Moreover, building large capacity will need huge investment delaying the payback period.

- A speciality product, on the other hand, can be launched with high price and good margins but may need brand building and huge R&D expenditure.

Decision Making Using Relevant Cost Concepts

- In decision making, one of the other ways is to classify the costs according to whether they are relevant or not to a particular decision.

- This concept is called Relevant Cost Concept and is valid and applicable for not only while planning an investment, but also while running a business, on the premises that decision making is a constant process and cost is an integral part of it.

- Why we call it a Relevant Cost is because the cost is not a fixed or onetime concept but a concept relevant at a given time for a given situation.

- It varies in total from one alternative to another.

- In fact, every business decision has its cost whether known, unknown, direct or indirect.

- Let’s now discuss in more detail various cost elements.

- Relevant costs are those future costs which will be affected by a decision whereas, irrelevant costs are those which are not affected by the decision.

- To give a simple example, if one owns both, a diesel and a petrol car, and he has to undertake a long journey, the decision about using diesel or petrol car will take into account the costs of petrol and diesel but not the cost of road tax and insurance, as these costs are already incurred and will remain the same, irrespective of the decision.

- So, the costs of petrol and diesel are relevant costs, while the costs of road tax and insurance are irrelevant cost.

- In this example, the costs of road tax and insurance are called “Sunk Costs” as these are made even before the decision making process starts.

- Sunk cost does not mean that it is a wrongly incurred expenditure or has no benefit. In our above example, road tax and insurance costs have to be incurred and have their benefits. The only point is that these are irrelevant to the decision of making a choice of using which of the cars.

- Relevant costs are also categorised as Avoidable costs, while the irrelevant costs are categorised under Unavoidable costs.

- This is because avoidable costs are incurred only if a specific business decision is made while the unavoidable costs will have to be incurred irrespective of the outcome of the decision.

- In our above example, the road tax and insurance costs are unavoidable costs while the cost of petrol and diesel are the avoidable costs.

- The relevant cost concept helps the decision making process by discarding the irrelevant cost data and thus, make the decision making process less complicated.

- While using the concept of Relevant costs, it is worthwhile to examine the so called “Opportunity Costs”.

- When you conceive a project, you had an alternative use available or was in mind which could have given you some X return.

- When you use the resources for another project, you will lose that opportunity and potential income. That lost income is the opportunity cost.

- It may be noted that opportunity cost, as a part of decision making, will arise only when use of Scares Resources is Involved.

Some of the important areas of decision making, which involve the Relevant Cost Concept, are as under:

- Add or drop a product line or segment:

- Make or buy decision

- Setting price of a product:

- Accepting or rejecting special orders

- Heavy discount offers from suppliers

- Import Substitutes

- Raw material mix

- Sale and Deals

- Outsourcing an activity or service

Relevant cost analysis plays a significant role in decision-making. Let us check out some relevant cost examples:

Example 1:

- The ABC Company plans to launch a self-care portal, which will result in a reduction of five positions within the company’s customer support department.

- In this case, the cost that is significant and relevant is the payment for the five personnel positions.

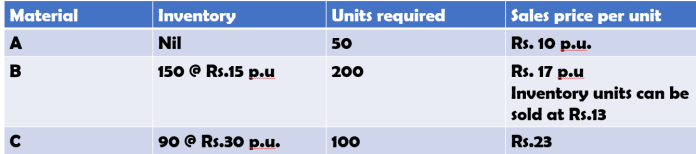

Example 2:

A business has received orders from buyer X for 3 materials A, B and C. It already has some old inventory of products B and C, as specified in the following table.

We have to arrive at the relevant cost of each material for making the decision of whether to sell or not.

Material A: With zero inventories, they will buy all 50 units at Rs. 10.

Hence, relevant costs = 50 units × Rs. 10 = Rs. 500

Material B: we will have to purchase 50 units @ 17/unit from the market to fulfil the order.

Hence, relevant cost of material B = Rs. 13 × 150 + Rs. 17 × 50 = Rs. 1,950 + Rs. 850 = Rs. 2800

Material C: Relevant cost of Material C = 100 units × Rs. 23 = Rs. 2,300

Example of Make or Buy Decision using Relevant Cost Concept

- A company that specialises in the production of completed items needs to have certain components.

- It must choose between manufacturing the components in-house or obtaining them from a third party.

- Naturally, the one with the lowest cost is the one to choose.

- In the case of a make or buy decision, some examples of associated costs are direct materials, direct labour, and other overhead expenses.

- Let’s say a business needs a component for a machine.

- They have the option of procuring the part from a third party or producing it in-house at the factory.

- In the event that the business chooses to outsource certain functions, it will need to free up some space that can be rented out.

- If the management decides to outsource work it can generate additional cash from rented premises.

- Thus, the company is able to reach the conclusion with the help of relevant cost analysis that purchasing the part is a more financially sound choice.

For example; The ABC Company is in the business of producing auto parts, some of which require very precise pieces of machinery.

- When purchasing from a supplier, the unit price is Rs. 5 (five rupees).

- However, the identical component can also be manufactured by the company itself.

- The company needs a total of 50,000 individual units of spare parts each year.

The following costs are incurred by the company when the goods are produced internally:

- Direct materials = Rs. 2/unit

- Direct labour = Rs. 2/unit

- Overhead costs = Rs. 1/unit

- Special tools = Rs. 40,000 Item

According to the above illustration, it will cost ABC Rs. 2,50,000 to buy from a supplier. And it will cost Rs. 2,90,000 to make the same internally. Therefore, ABC should continue outsourcing.

Example of Continue Production or Close Business Unit decision, using Relevant Cost Concept

- The question of whether or not to continue operations or to shut down individual business units, inevitably arises at some point in the life of every company.

- In this case, the management needs to assess whether or not the units produced are generating the desired income and whether or not the maintenance cost of the plant and machinery is high.

- When it comes to making that decision, having the appropriate cost analysis form is of the utmost importance.

For Example The company Amol makes cheese worth Rs. 10,000 per month.

- Maintenance cost for machinery is Rs. 3,000,

- Rs. 2,000 for material,

- Rs. 2,500 for labour, and

- Rs. 2,500 for miscellaneous costs.

- Overall expenses amount to Rs. 10,000 for an income of the same amount at Rs. 10,000.

- So, the company might think of discontinuing the cheese unit.

- Amol might continue with cheese production if the expenses are lower, like Rs. 7,500/-.

Decision Making Using Activity Based Costing (ABC)

- Prior to the emergence of ABC, companies typically calculated profitability using the allocation method.

- This allocation method involved allocating costs to a product or customer using metrics such as the total number of units produced, accounts, customers, or transactions.

- Activity Based Costing (ABC) is used for estimating the cost which in turn is used for decision making.

- It has been widely used to help the management in taking important decisions like pricing, outsourcing etc.

- The method is used for costing of products, service or even a customer who is being serviced, all termed as objects under this method.

- The method is named after activity, which is the focus of the process.

- ABC method of costing is based on the fact that the products and services, provided by a company to its customers, involves various such activities which are not exclusively related to one product or service.

For example: The quality control department ensures that all the products and services provided by the company are of desired quality.

- But the service provided by this department is not equally spread over all such products and services.

- Activity-Based Costing (ABC) is technique of appropriately assigning the costs of such activities to various products and services of the company.

- ABC involves identification of each cost driving activity and apportioning its cost to different products or jobs.

- The basis for this allocation is the quantity of each such cost driving activity required for their completion.

- Under this technique, the overhead costs of the company are identified with each cost driving activity.

Example: Company SW Ltd purchases CKD (Completely Knocked Down) packs of 2 wheelers and 3 wheelers and assembles them to sell in the market.

- The material and labour cost of each pack, till it reaches the assembly line, is Rs. 50,000 and Rs. 80,000 respectively.

- Total cost incurred by assembly line, during the year, is Rs. 20,00,000, utilising 20,000 labour hours.

- Assembly of a 2 wheeler takes, on an average, 20 labour hours while the assembly of a 3 wheeler takes 30 labour hours. We have to find the cost of each 2-wheeler and 3wheeler using the ABC costing method.

Solution:

- Direct cost of material and labour for each pack is known, viz. Rs. 50,000 and Rs. 80,000 respectively.

- In the activity of assembly, the main cost constituent (cost driver) is the labour, which is paid on hourly basis.

- Rate of the cost driver is total assembly cost/labour hours used = 20,00,000/ 20,000 = Rs. 100 per labour hour.

- So, the assembly cost allocated to each 2-wheeler is Rs. 20*100 and for 3-wheeler, it is Rs. 30*100.

- So, the total cost of each 2-wheeler is Rs. 52,000 and that of each 3 wheeler, Rs. 83,000.

Methodology of Activity Based Costing Method

- The basis of attribution of cost can be the benefit received from the indirect activates.

- The cost attribution can also be based on the activities undertaken to produce each product or service.

The following terms are used while operating ABC System:

- Cost Object. This is an item for which the cost measurement is required and it can be a product, service or a customer.

- Cost Pool: This term is used for grouping of the costs incurred on a particular activity which drives them

- Cost Driver. This is any factor that causes a change in the cost of activity. These are further classified into Resource Cost Driver and Activity Cost Driver.

- ABC method can give us product profitability as well as customer profitability.

- It can also throw light of process efficiency. In short, activity-based cost information is both intuitive and logical.

- To conclude, it makes sense to those charged with the task of improving performance and the method provides them with transparent information on the cost ramifications of their decisions.

![]()

ILLUSTRATION

Let’s say that the management of a company that manufactures certain electronic devices has taken a decision to install an ABC system. The management comes to the conclusion that there should only be three cost drivers for all overhead expenses, and those are direct labour hours, machine hours, and the quantity of purchase orders. The following are the company’s overhead costs, as shown in the general ledger: –

Differentiate which overheads are driven by direct labour hours?

Similarly, overheads driven by machine hours include Machine maintenance, depreciation and Electricity totalling Rs. 2,500 and finally overheads driven by number of purchase orders include purchasing department labour and purchasing department supplies totalling Rs. 4,250. Now, overhead rate is calculated by the formula Total cost in the activity pool ÷ Base, base being the total number of labour hours, machine hours and total number of purchase orders in the given case. Assume that the total number of labour hours be 1,000 hours, machine hours be 250 hours and total purchase orders be 100 orders. So, Cost driver rate would be

Character-Based Decision-Making Model

- There are many models which suggest framework for deciding the ethical soundness of a decision.

- Prominent among them is the Character-Based Decision-Making Model, developed by Josephson Institute of Ethics.

- It provides a framework that can be used to decide whether a decision is morally and ethically sound.

The pillars of this model are:

- Trustworthiness,

- Respect,

- Responsibility,

- Fairness, and

The model suggests a seven-step path to better decisions.

These steps are:

- Stop and Think

- Clarify Goals

- Determine Facts

- Develop Options

- Consider Consequences

- Choose

- Monitor and Modify

The model suggests the rationalization of obstacles to ethical decision making, as under: rationalizations

- If It’s Necessary, It’s Ethical

- The False Necessity Trap

- If It’s Legal and Permissible, It’s Proper

- It’s Just Part of the Job

- It’s All for a Good Cause

- I Was Just Doing It for You

- I’m Just Fighting Fire with Fire

- It Doesn’t Hurt Anyone

- Everyone’s Doing It

- It’s Ok if I Don’t Gain Personally

- I’ve Got It Coming

- I Can Still Be Objective

The model involves the Golden Rule – “Help when you can and avoid harm when you can.”

It also involves the principle that, in general, the company should make decisions that promote the greatest amount of moral justness.

Download PDF

CAIIB Paper 3 Module B Unit 6- Decision Making (Ambitious_Baba)

- Click here to Fill the form for Free CAIIB Study Materials

- Join CAIIB Telegram Group

- For Mock test and Video Course Visit: test.ambitiousbaba.com

- Join Free Classes: JAIIBCAIIB BABA

- Download APP For Study Material: Click Here

- Download More PDF

Buy CAIIB MAHACOMBO